If you want to subscribe to only the Infuse quarterly letters, make sure to navigate to your profile → manage subscription → turn off all notifications besides Infuse.

If you’re receiving this email twice as you subscribed on the infuse-am.com site, feel free to unsubscribe here.

Dear partners,

Thank you for your continued trust and support; you are the best partners I could ask for.

At the end of the day, good investing is about understanding reality. If you deeply understand a situation, you will know what to do. However, the future is unpredictable so understanding, alone, doesn’t guarantee success but rather informs probabilities. Our primary job is to find situations where the probabilities are extremely in our favor. One probability-tilting characteristic is buying a stock at a low multiple of cash flow. Just blindly buying a low multiple stock is not good investing but it does tilt the odds in your favor. However, if you’re buying a business and expect to get paid back from cash flow, longevity and business quality matter immensely. After all, if you pay 10x cash flow on a stagnant business, it has to survive at least ten years for you to make money. This is a simple yet important insight. So a dominant competitive position and a moat definitely tilt the odds in your favor. Buying a truly scarce asset is a good way to not lose money because there will likely be a bid for that asset. But if an asset is easy to replicate, by definition, it won’t be as valuable. Another factor that improves odds is management alignment. As public market investors, we don’t have the whole story, no matter how good your scuttlebutt is. Trusting a management team with a track record of fleecing investors severely handicaps the odds of success. Further, strong financial footing helps quite a bit. If a company is profitable without debt, it’s awfully hard to go bankrupt. Sure, things will change over time but that’s where the irreplaceability and moat come into play. With a robust financial foundation, you seriously decrease the odds of a disastrous outcome. We could go on and on, but the goal is to see reality for what it really is and in doing so, improve your odds drastically. If you can find a company that is hard to replicate with an aligned manager, a strong financial picture, at a low multiple of cash flow, that is a great start to stacking the deck in your favor. But that’s also like saying ice cream is tasty. Of course it is! What actually matters is putting these concepts into practice. Those criteria are an example of our map but the map is not always the terrain. In reality, businesses are messy and we have to make probability-weighted decisions based on incomplete information. The ideal scenarios are when your research says the odds of success are much higher than the market is expecting. Variant perception is at the heart of good investing but it’s also incredibly difficult. If the herd is running one way, that is usually toward safety. Making a bet that the majority isn’t seeing reality clearly is daunting. It requires constant paranoia of trying to see blind spots. One great quote about this concept is from Henry Ford:

“Even the man who most feels himself ‘settled’ is not settled — he is probably sagging back. Everything is in flux, and was meant to be. Life flows. We may live at the same number of the street, but it is never the same man who lives there. It could almost be written down as a formula that when a man begins to think that he at last has found his method, he had better begin a most searching examination of himself to see whether some part of his brain has not gone to sleep.”

With all of that said, I want to talk a little bit about one of our top positions and how we thought the odds were tilted in our favor. We started buying Intellego at around a $60 million USD valuation. The CEO owned about 10% of the shares but there had been a string of questionable governance things like a board member being convicted of insider trading, a part-time CFO, and very promotional press releases. At the time, the company was doing about $8 million in EBIT, had about $6 million in inventory/fixed assets, $8 million in receivables net of payables, and a negligible amount of debt. I figured that even if they got a 50% haircut on the working capital, the true enterprise value was about $53 million on $8 million in EBIT. Receivables were still too high but they also signed some very lenient contracts in the early days just to get traction. The main thing I needed clarity on was how difficult it would be to replicate the dosimeter business. Well, it turned out that the patent on the photochromic ink had just been continued, a huge German client had been doing trials for well over a year, and there were rumblings of a billion dollar Chinese distributor interested in an exclusive deal. Still, it was not clear that dosimeters would be used every day in hospitals and manufacturing. After all, why were receivables so high if the products were being used constantly? Surely, hospitals were just trying the dosimeters and then not paying quickly because the product was not mission critical? These questions are what I spent hours on, trying to see reality as clearly as possible. Quite honestly, I couldn’t get complete satisfaction. Different users had different opinions, different hospitals had different protocols, and different countries had different disinfecting regulations. But even with incomplete information, on the downside, I thought the company had decent odds of lasting more than six years and in an upside scenario, had the potential to grow its earnings by at least an order of magnitude. These asymmetries don’t come along very often so when they do, betting big can make sense. At the same time, extreme paranoia is warranted because surely, I must’ve been missing something! I talked to every bear I could and tracked down as many answers as possible. I don’t say all of this to pat myself on the back but rather dive into a real-life example of seeing reality as clearly as we can and translating that into probabilities. At a very high level, I thought the odds of fraud were about 10%, there was a 10% chance the stock could go up 20x, a 30% chance it would get bought out at its current value, and another 50% chance it could triple in price. These were very rough estimates and they were and are still changing but the expected value was nearly 4x over a 5-year timeframe.

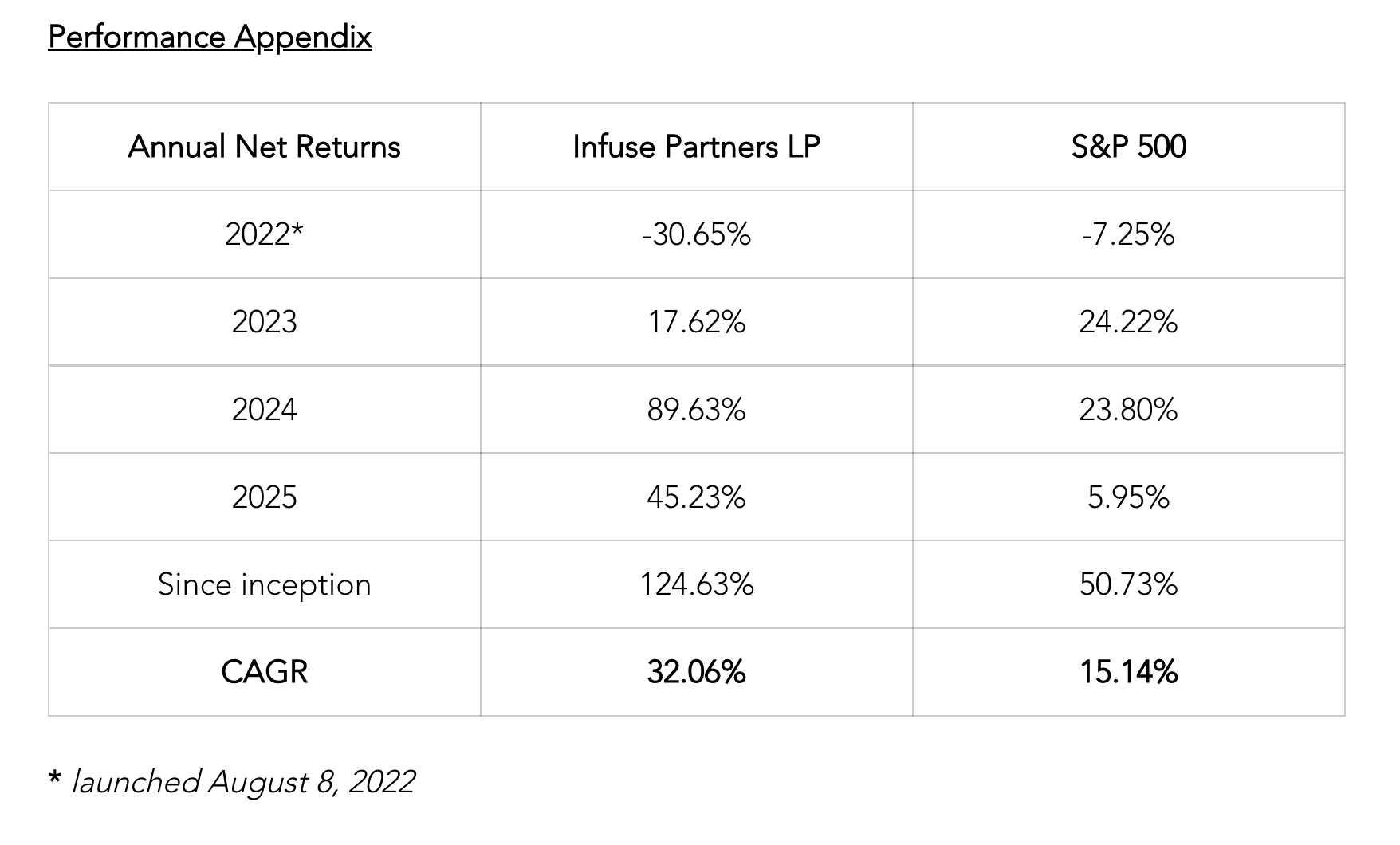

At the end of Q2, Intellego was at a ~$258 million USD market cap and its trailing EBIT is roughly $27 million, or a 9.5x EBIT multiple. That is just two turns (~7.5x initial EV/EBIT) higher than where we bought it, even though the stock has more than tripled from our average price. These situations, where we make money through earnings growth, are exactly what we are looking for. Some people are great at playing the perception game. But what is proven to move stock prices over the long run is earnings growth. Trying to tilt the odds in our favor by studying growth runways, business quality, and valuation is our formula for success. We have made many mistakes since the start of the fund but I’m happy to share how the Intellego thesis developed and how we grew your hard-earned capital through this experience. As the world continues to change, we will focus exclusively on how to tilt the odds in our favor.

Closing

I’m honored to have you as a partner. Thank you for your trust and support. It enables me to think long-term and will be our own competitive advantage.

The stock market, like life, will have its ups and downs. All we can do is focus on what we can control and work hard to continually raise our standards. Our strategy is simple – hitch a ride to the world’s best entrepreneurs who are running the fastest-growing, highest-quality companies at the most attractive valuations we can find. Here’s to many more years of focusing on the inputs and letting the outputs take care of themselves.

Sincerely,

Ryan Reeves

Disclosures

Infuse Asset Management LP (“Infuse”) is an investment management company to a fund that is in the business of buying and selling securities and other financial instruments. This information is provided for informational purposes only and does not constitute investment advice or an offer or solicitation to buy or sell an interest in a private fund or any other security. An offer or solicitation of an investment in a private fund will only be made to accredited investors pursuant to a private placement memorandum and associated documents.

Infuse may change its views about or its investment positions in any of the securities mentioned in this document at any time, for any reason or no reason. Infuse may buy, sell, or otherwise change the form or substance of any of its investments. Infuse disclaims any obligation to notify the market of any such changes.

The S&P 500 is a U.S. equity index. It is included for informational purposes only and may not be representative of the type of investments made by the fund. References made to this index are for comparative purposes only. Reference to an index does not imply that the funds will achieve returns, volatility, or other results similar to the index. The fund’s portfolios are less diversified than this index. Returns for the index are total returns which include dividends and do not reflect the deduction of any fees or expenses which would reduce returns.

An investment in the fund is speculative and involves a high degree of risk. The portfolio is under the sole trading authority of the general partner. An investor should not make an investment unless the investor is prepared to lose all or a substantial portion of its investment. The fees and expenses charged in connection with this investment may be higher than the fees and expenses of other investment alternatives and may offset profits.

The information in this material is only current as of the date indicated and may be superseded by subsequent market events or for other reasons. Statements concerning financial market trends are based on current market conditions, which will fluctuate. Any statements of opinion constitute only current opinions of Infuse which are subject to change and which Infuse does not undertake to update. Due to, among other things, the volatile nature of the markets, an investment in the fund/partnership may only be suitable for certain investors. Parties should independently investigate any investment strategy or manager, and should consult with qualified investment, legal and tax professionals before making any investment.

The fund is not registered under the Investment Company Act of 1940, as amended, in reliance on an exemption thereunder. Interests in the fund have not been registered under the securities act of 1933, as amended, or the securities laws of any state and are being offered and sold in reliance on exemptions from the registration requirements of said act and laws.